For a vibrant economy, the payment system presents a substantial component of the country's infrastructure system. Developments in information technology and changes in laws, regulations and institutions in Bhutan has encouraged the rise of new payment instruments and delivery channels as well as processing arrangements for low & large value, time-critical and instant payments. We can therefore expect more major changes in the payment systems in the next five years than we have in the last five decades. Hence, developing a safe and robust payment system infrastructure that enables the efficient functioning of economic activities, while promoting financial innovation has always been one of the foremost priorities for the RMA. Ergo, on the domestic front, the RMA has enhanced the domestic system - from EFTCS to GIFT payments, a platform based on the latest and futuristic technologies called Global Interchange for Financial Transaction (GIFT) launched in July 2019.

On the regional side, the historic connection of Bhutan Financial Switch with the National Financial Switch of India was jointly launched by His Excellency Shri Narendra Modi, Prime Minister of India and His Excellency Dr. Lotay Tshering, Prime Minister of Bhutan on 17th August 2019. The integration allows acceptance of RuPay cards issued by Indian banks at the ATMs and POS terminals in Bhutan. The RuPay cards issued by banks in Bhutan for acceptance in India will be enabled during the second Phase of the project.

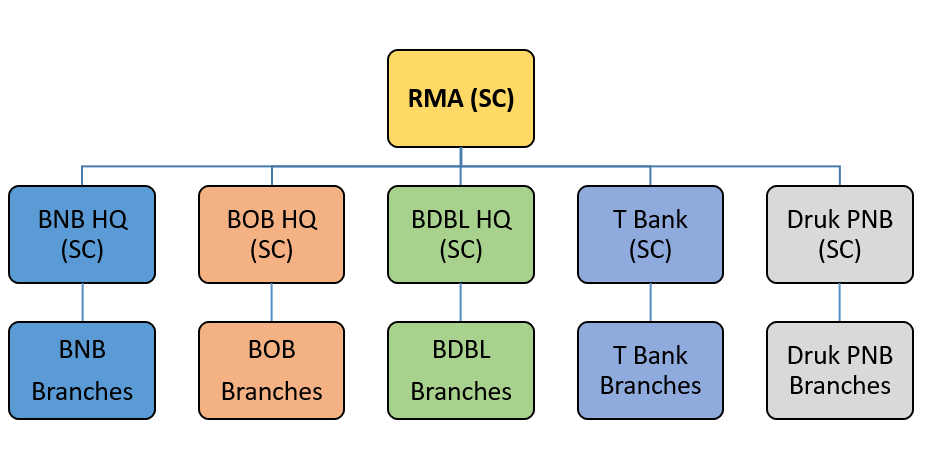

With a view to inter-connect the ATMs, POS in the country and facilitate easy banking for the common citizen, the RMA proposed the idea of implementing the Bhutan Financial Switch (BFS). The Bhutan Financial Switch (BFS) would facilitate connectivity between the Bank's Switches, and create inter-bank payment gateways for various e-commerce transactions and activities both domestic and international.

2 December, 2011 : BFS ATM was launched by Hon'ble Prime Minister of Bhutan. Ever since the introduction, BFS has facilitated interoperability for the ATMs in the country.

12 July, 2012: BFS POS was launched by Hon'ble Finance Minister. The POS service addition to BFS has facilitated interoperability of entire POS network in the country.

In the early 80s and the 90s, most of the financial transactions were carried out through CASH/cheques in the country. However, with the advent of ATM and POS machines in the mid 2010s, execution of financial transactions has moved from paper to electronic. Now in the age of the internet and the technology, things are becoming FAST, SECURE and REAL TIME; people no longer prefer going to the banks, they rather prefer doing it ONLINE - "mobile apps/wallets". For example, in the developed economy, a customer can open a bank account through a mobile app without having to visit the bank and repeating the KYC procedure. Further, all utility expense are also made online. This has simplified the way we live today.

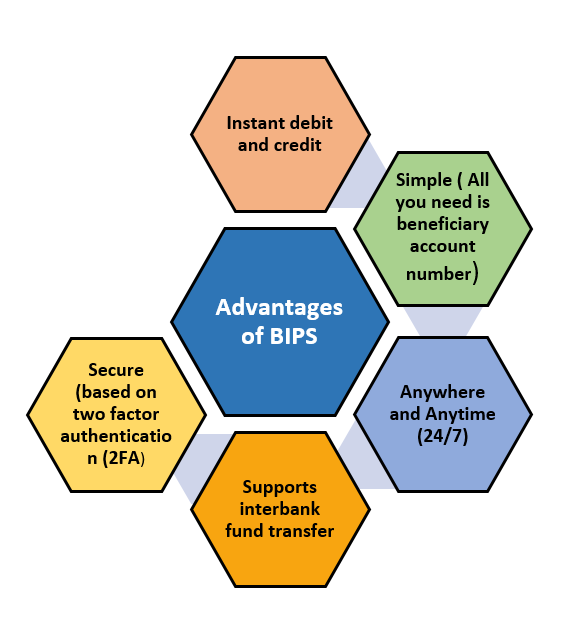

Likewise, the RMA has initiated a mobile app based payments network. Which is an important initiative to promote the usage of digital payments in the country – BIPS (Bhutan Immediate Payment Service) empowers customer to send money through different channels, such as Internet banking, mobile apps, and ATMs, to a receiver in any other participating banks. The system is managed by the Royal Monetary Authority of Bhutan by interconnecting all the member banks - BOB with mBoB; BNB with mPAY; BDBL with ePay; T Bank with TPAY; and Druk PNB with PNB mobile app. These apps also allow payment for expenses such as Utility bills, various taxes, insurance and loan, phone bills, etc. Additionally, RMA has initiated QR code payment at fuel stations, shops and vegetable markets in the country.

Further, BIPS added the Payment Gateway functionality to allow various types of e-commerce and m-payments, such as citizens-to-government (C2G), business-to-business (B2B), government-to-citizens (G2C), etc. BIPS was publicly launched on 27th January 2017.

17th July, 2020 : The RMA has also launched Bhutan QR based payment options, wherein the consumers/users can make the payments at the merchant location by scanning the merchant QR templates. With the launch of Bhutan QR, a customer having account with any bank could make payments to merchants belonging to any bank.

What is a payment gateway? A payment gateway or PG is "a gateway used to exchange transaction data between the merchant and the acquiring bank. This gateway serves as an interface between the payment form on the merchant's website and an acquiring bank". All the information is encrypted to maintain secure exchanges. A payment gateway is the channel that allows payment instructions to flow from a payer to a merchant. The information is shared between an issuing bank, a merchant, a card holder, and an acquiring bank.

The RMA in collaboration with the member banks, and DITT, MoIC launched the RMA PG on 27th January 2016, to promote the use of digital payments and to provide access to financial service by harnessing the use of Information Communication Technologies (ICTs). Under this initiative, a customer is enabled to avail G2C services and to initiate inter-bank fund transfer and payments on an instant, secure and real-time manner with any of the participating banks. It provides interoperability of payments across the banks and agencies and facilitates e-payments between Citizens-to-Government, Government-to-Citizens, Business-to Business, etc.

Further, with the view to promote and harness the use of digital payments, the International Payment Gateway by BOBL was launched in 2016 and BNB in 2019, to offer e-Commerce services to the local business merchants in the country by providing international card acquiring services for VISA/MASTER/American Express branded card schemes. The merchant types mainly included products and services related to Textile business, import and export, travel agencies, IT Firms, hotels etc. where the international clients could avail these services by making payments online through their portals.

In addition, IPG requires businesses to have a website to establish the payment option link. Once the payment option is established on their website, product and services can be purchased by international clients.

If you wish to apply and register for the PG license, visit :17 August 2019 : His Excellency Shri Narendra Modi Prime Minister of India and His Excellency Dr. Lotay Tshering Prime Minister of Bhutan, jointly launched the RuPay card scheme in Thimphu. Bhutan is now the second country to accept the RuPay. Through this initiative, Indian visitors can use their RuPay cards at the ATM and POS machines in Bhutan. Besides, this facility would be available for Bhutanese travelers and students in India.

The service can be accessed on ATMs and POS terminals of all the Bhutanese Banks across the country. Besides, Indian visitors should ensure their card is enabled for use in Bhutan by their ISSUER bank in India.

The withdrawal limit per transaction is Nu. 10,000 as set by the acquirer banks in Bhutan and the permissible aggregate withdrawal in a day is capped by the issuer bank in India.

Mobile money/ e-money/ mobile wallet enables individuals to use their mobile phone to top-up, pay bills, remit funds, cash in- cash out and save, similar to the mobile applications owned by the banks; but most often mobile money/mobile wallets are issued by telecommunications companies. As such, in Bhutan, we have two authorized e-money issuer : B-Ngul (Bhutan Telecom) and e-teeru (Tashicell), both issued by Telecos.

The main objective is to reach out to the unbanked population of the country, as a part of financial inclusion.

Royal Monetary Authority started the first ever Clearing House in 1997 in Thimphu and another Regional Clearing House at Phuntsholing in 2000. Due to its legacy system and processes, clearing and settlement took T+2 or even more leading to delay, loss of Cheque, customer complain and many more.

Hence, in 2007, RMA with assistance from Asian Development Bank implemented Cheque Truncation System (CTS), whereby paper-based clearing of cheques in the country have been replaced by image-based processing and settlement. Further in the year 2017, Cheque Truncation System was streamlined to ensure timely reconciliation and settlement. Thus, the delays associated with the physical movement of cheques was avoided as the bank branches across the country would initiate scanning the interbank cheques making the settlement T+1.

Currently, the Department of Payment and Settlement has the following rules and regulations in place to ensure safety, efficiency and integrity of the payment systems in the country :

*Note : Any charges related to the above mentioned systems can be viewed on https://www.rma.org.bt/notificationdirectives.jsp?id=8